The 17 Schedule C Expense Categories — Which Ones Apply to Your Business

Schedule C lists business expense categories for self-employed filers. What each one covers, which apply to most freelancers, and which are rarely used

Schedule C expense categories are the IRS's taxonomy for self-employment deductions. When you file a federal tax return as a sole proprietor, freelancer, or single-member LLC, Part II of Schedule C is where you report business expenses. Each goes on a named line for that expense type. The category you use affects how the IRS reads your return, which is why it's worth understanding what each one covers before you file.

Most self-employed people use five or six of these categories consistently. A few apply only to businesses with employees, vehicles, or physical inventory. Some are rarely used by anyone outside specific industries. This article walks through each so you know where your expenses belong and which categories you can safely ignore.

Line 8 — Advertising

Expenses for promoting your business: paid ads on Google, Meta, or Instagram; sponsored content; business cards and printed materials; signage; promotional merchandise; fees to a marketing agency. Any cost that exists specifically to attract customers counts.

This is one of the most universally applicable categories. If you've spent money on any form of marketing, it goes here.

Line 9 — Car and truck expenses

If you use a personal vehicle for business, you have two options: the standard mileage rate (a flat per-mile deduction set by the IRS each year) or the actual expense method (a percentage of real vehicle costs including gas, insurance, maintenance, and depreciation, based on business-use percentage). You choose one method for a vehicle and generally stick with it.

Commuting (driving from home to a regular workplace) does not qualify. Business mileage means travel to clients, job sites, supply runs, meetings, and similar business purposes.

This is also one of the largest categories for many self-employed people. Track every business trip.

Line 10 — Commissions and fees

Payments to other people who are not your employees that function as part of making sales: sales commissions to independent reps, referral fees, finder's fees, broker fees on transactions. Does not include payments to contractors for services (that's Line 11). Commissions and fees are specifically tied to sales activity.

This line is common for anyone using sales networks, affiliate arrangements, or paying referrers.

Line 11 — Contract labor

Payments to independent contractors and freelancers you hire for your business. If you paid a contractor $600 or more in the year, you're also required to file a 1099-NEC. Employees belong on Line 26 (Wages). This line is specifically for non-employee labor.

Common examples: a freelance designer, a contract bookkeeper, a hired assistant, a subcontractor on a project.

Line 12 — Depletion

Depletion applies when your business extracts a natural resource such as oil, gas, timber, or minerals. It accounts for the gradual using-up of those finite resources over time, functioning like depreciation for extracted materials.

Unless your business involves natural resource extraction, this line doesn't apply to you. Most freelancers, consultants, and service providers will skip it entirely.

Line 13 — Depreciation and Section 179

When you buy equipment, machinery, furniture, or other business property that lasts more than a year, the cost typically can't be deducted all at once. Depreciation spreads that cost over the asset's useful life. Section 179 is an election that lets you deduct the full purchase price of qualifying property in the year you buy it rather than spreading it across years.

Common uses: computers, cameras, machinery, office furniture, tools, and equipment. Vehicles can also be depreciated here (or on Line 9, depending on how you're handling the vehicle).

Most self-employed people who buy significant equipment will encounter this line. If you've purchased a laptop, a camera, or specialized tools for your business, depreciation likely applies. In fact, most self-employed people who bought a laptop, phone, or piece of equipment for their business this year have a Section 179 claim. They just don't know it.

Line 14 — Employee benefit programs

Benefits you provide to employees: health and dental plan contributions, accident and disability coverage, dependent care assistance, educational assistance, and similar programs. This does not cover health insurance for the self-employed person themselves. That deduction appears elsewhere on the return, not on Schedule C.

If you have no employees, this line is blank.

Line 15 — Insurance (other than health)

Business insurance premiums: general liability, professional liability (errors and omissions), property insurance, business interruption coverage, commercial auto. This is insurance that protects the business, not personal or health coverage.

Common for: consultants and service providers with E&O coverage, contractors with liability insurance, photographers and other creative professionals.

Line 16 — Interest

Split into two sub-lines: mortgage interest on property used for business (16a) and other business interest (16b). The second covers interest on business loans and business credit cards.

If you have a business bank account with a credit card, the interest you pay on that card goes here. Interest on personal credit cards used for business expenses does not qualify. The account must be a business account. Interest on a home mortgage taken for a home office is complicated; a CPA is worth consulting before claiming it.

Line 17 — Legal and professional services

Fees paid to attorneys, CPAs, accountants, bookkeepers, and other licensed professionals for services related to your business. Tax preparation fees that relate to your Schedule C also go here.

Common uses: attorney fees for contract review, accounting fees for bookkeeping or tax preparation, consulting fees to professionals.

Line 18 — Office expense

Day-to-day supplies and services needed to run the office side of your business: postage, paper, pens, printer ink, small software subscriptions, and similar consumable items. This is distinct from larger equipment purchases (Line 13) and general business supplies (Line 22).

The line that tends to cause confusion: software subscriptions. A monthly SaaS tool used for your business generally lands here. Large software purchases or annual licenses may be better handled on Line 13 under Section 179. If the amount is significant, ask a CPA.

Line 19 — Pension and profit-sharing plans

Contributions you make to retirement plans you've established as a self-employed person: a SEP-IRA, SIMPLE IRA, or solo 401(k). The deductible amount has annual limits set by the IRS.

This line is relevant if you're actively contributing to a self-employed retirement plan. If you're not, skip it.

Line 20 — Rent or lease

Two sub-lines: vehicles, machinery, and equipment you rent or lease (20a), and other business property you rent (20b). If you lease your office space or a studio, it goes on 20b. Equipment rental for a project goes on 20a. Owning the equipment means depreciation on Line 13 instead.

Line 21 — Repairs and maintenance

The cost of keeping business property in working condition: equipment, a business vehicle, leased space. Not improvements or additions (those are capital expenditures that belong on Line 13), but ordinary maintenance: having your business laptop repaired, getting a vehicle oil change, fixing a piece of equipment.

Line 22 — Supplies

Materials and supplies directly used in producing your product or delivering your service. For a photographer: memory cards, printing supplies, cleaning kits. For a contractor: materials purchased for a job. For a caterer: disposable supplies for an event. For a consultant who mostly sells time: this line is typically minimal.

This is the cost of goods and materials that go into the work itself, not office supplies (Line 18) or equipment (Line 13).

Line 23 — Taxes and licenses

State and local business taxes, business license fees, professional license renewal fees, and real estate taxes on business property. Federal income taxes do not belong here. Self-employment tax doesn't go here either. It's handled elsewhere on the return.

Common uses: annual business license renewal, professional licensing fees, local business taxes.

Line 24 — Travel and meals

Split into two components. Business travel expenses (flights, hotels, ground transportation for business trips) go on one line. Meals related to business go on a separate line, and only 50% of the meal cost is deductible.

The IRS distinguishes carefully here: the trip must have a genuine business purpose. A conference in another city qualifies; a personal vacation with a business call tacked on does not. For meals, the business purpose must be clear: meeting with a client or business associate, travel meals during a business trip.

This is one of the more audited categories. Keep records that document the business purpose, who was present, and what was discussed.

Line 25 — Utilities

Utility costs for your business location: electricity, gas, water, internet, phone. If you work from a dedicated home office, the portion of your home utilities attributable to the office may be deductible, but only the business-use percentage.

For a standalone business location, all utility costs qualify. For home-based businesses, the calculation requires determining what percentage of your home is used exclusively for business.

Line 26 — Wages

Salaries and wages paid to employees. If you have no employees, this is blank. Independent contractors and freelancers are Line 11, not Line 26.

Line 27 — Other expenses

A catch-all for ordinary and necessary business expenses that don't fit any of the specific categories above. Listed separately on a supporting schedule. Common examples: professional development and training directly related to your trade, industry-specific software, professional association dues, bank fees on business accounts, subscriptions to trade publications.

The key test is whether the expense is "ordinary and necessary" for your specific type of business. An expense is ordinary if it's common in your industry. It's necessary if it's helpful and appropriate for your business, not optional luxury spending.

Which categories apply to most self-employed people

For a freelancer, consultant, or service-based sole proprietor, a typical year involves six to eight of these categories:

- Advertising (Line 8): if you run any paid promotion

- Car and truck expenses (Line 9): if you drive for work

- Contract labor (Line 11): if you hire anyone freelance

- Depreciation (Line 13): if you buy equipment

- Insurance (Line 15): if you carry liability or E&O coverage

- Legal and professional services (Line 17): accounting and legal fees

- Office expense (Line 18): software subscriptions and consumable supplies

- Travel and meals (Line 24): if you travel for clients or attend conferences

- Other expenses (Line 27): training, dues, bank fees

Depletion, employee benefits, pension contributions, wages, and rent or lease only apply if your business involves those specific things. You're not expected to have something in every category.

Connecting categories to records

Knowing which category applies is one piece. The other is having the records to support the deduction: date, amount, vendor, and business purpose.

Self-employed people often lose deductions not because they spent less than they think, but because they can't reconstruct the records at tax time. Expenses tracked at the moment of purchase, with a receipt, a category, and a brief note on the business purpose, are far easier to defend than expenses reconstructed from bank statements months later.

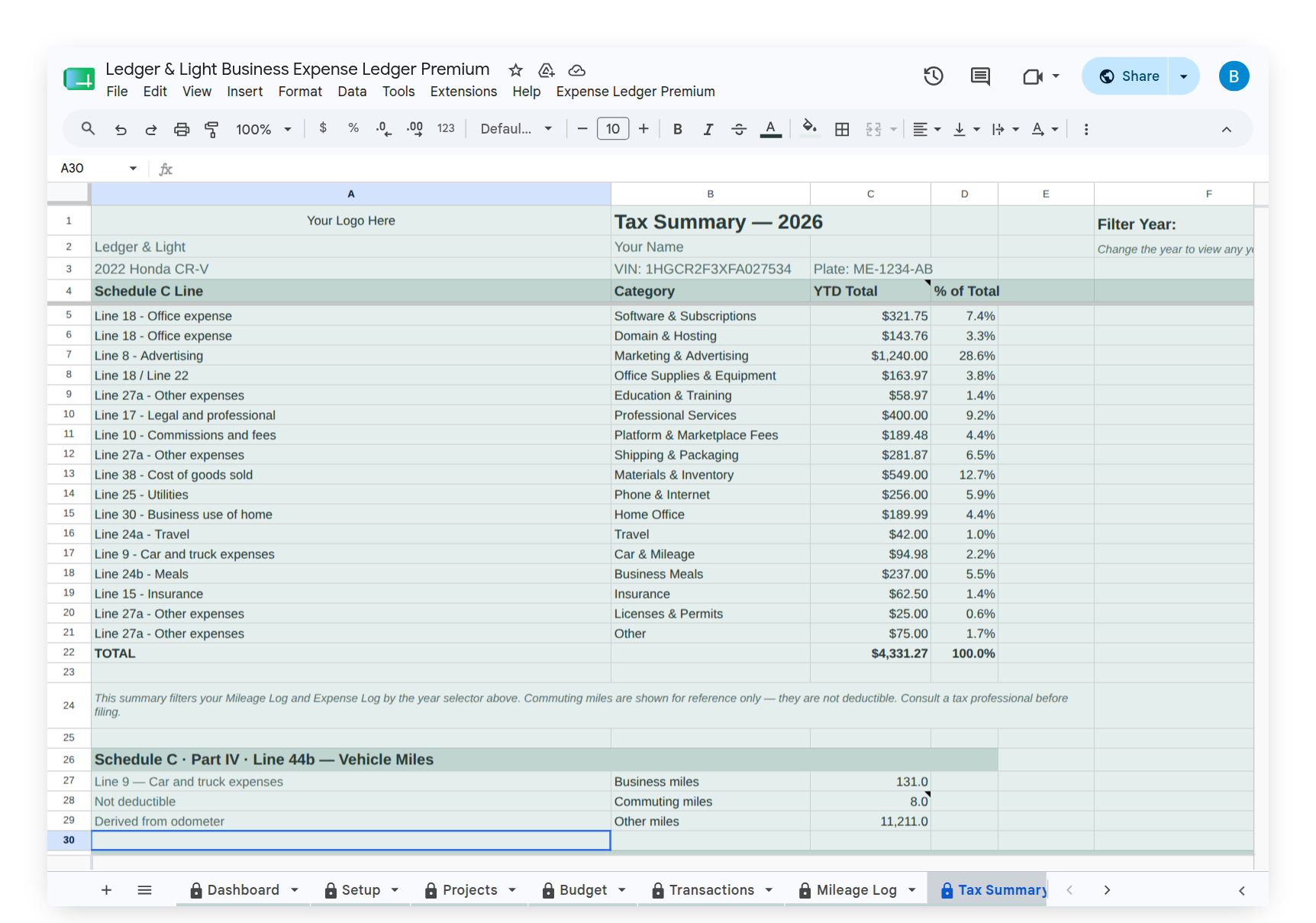

Your Expense Ledger organizes expenses across these 17 Schedule C categories from the moment of entry. Every expense logged through the Expense Form arrives pre-categorized. The form includes a category dropdown mapped to all 17 lines, a receipt photo field for attaching an image at the point of purchase, and enough fields to capture what the IRS wants to see. The Tax Summary shows category-by-category totals ready for Schedule C. On Premium, the Email Tax Report sends your Tax Summary, expense transactions, and mileage log directly to your accountant as formatted PDFs, and Tab Export saves any tab to your Drive by year.